Market & Economic Commentary: Q4 2025

Closing the Year: Market Review and Perspective

Overview

2025 marked the third year in a row of double-digit stock market gains as the U.S. market, measured by the S&P 500, gained 16.4%. Global markets also rose, in many cases outpacing the US markets. Similarly, in the fourth quarter, the US market rose 2.4% while global markets outside the US delivered 5%, highlighting the benefits of global diversification. Despite periodic uncertainty throughout the year, market strength was supported by easing monetary policy, resilient corporate earnings, continued economic growth, and a further moderation in inflation.

U.S. Equity Markets

U.S. markets demonstrated notable resilience in Q4 despite several headwinds, including concerns around a prolonged government shutdown, weakening consumer sentiment, and emerging labor market softness. Although markets experienced some late-quarter volatility, U.S. equities reached all-time highs during the period.

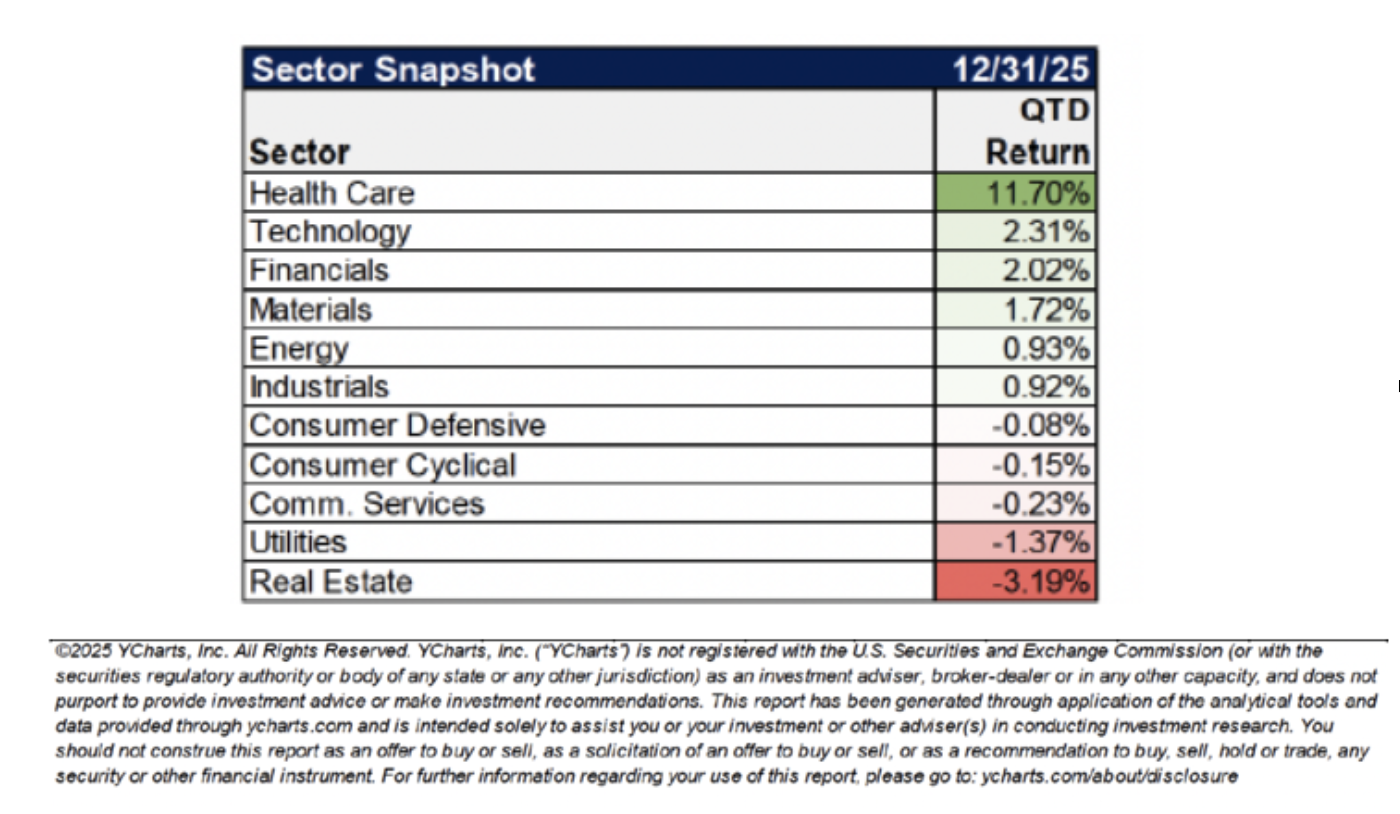

Market leadership broadened during 2025. Five of the so called “Magnificent Seven” stocks underperformed the S&P 5001, revealing potential vulnerabilities in highly concentrated, mega cap heavy portfolios. Elevated equity valuations of certain sectors, particularly technology, remained a point of concern as price to earnings ratios approached historical highs. Questions about potential over-investment in Artificial Intelligence (AI) infrastructure added a drag to some related sectors and propelled an investment shift to other industries. Health Care, in particular, posted a strong quarterly gain of nearly 12%, benefiting from defensive characteristics and improved earnings visibility. Markets also responded favorably to the Federal Reserve’s continued cutting cycle during the quarter.

Tech Stocks Took Second Place in Q4 2025

International & Emerging Markets

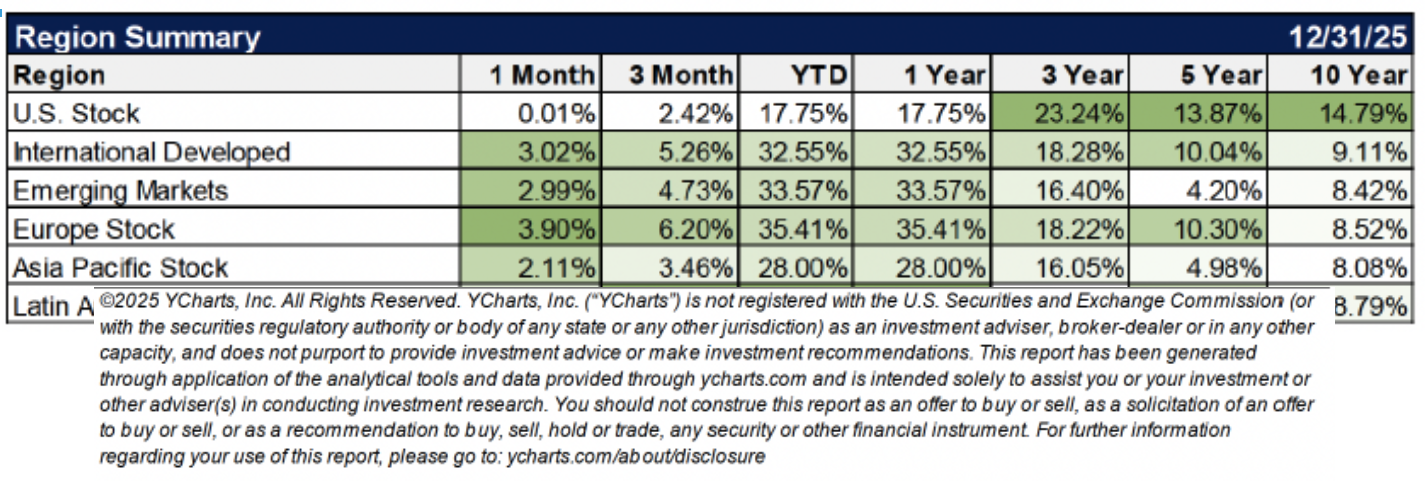

International equities were a clear bright spot in Q4 and throughout 2025. Both developed and emerging markets posted strong returns, supported by a weaker U.S. dollar, improving global economic data, and renewed capital flows into nonU.S. markets. Emerging markets benefited from stronger commodity exports, and easing inflation pressures

Valuations abroad remained more attractive relative to the U.S., contributing to strong performance across Europe, Asia, and emerging economies. The year reinforced the value of maintaining global exposure rather than relying solely on U.S.centric portfolios.

International Markets Outperformed the US Market in 2025

Economic Growth and Lower Interest Rates Support the Market

Economic data in late 2025 presented a mixed but generally supportive backdrop.

The U.S. unemployment rate rose to 4.6% in November, the highest level since early 2021, signaling some cooling in labor conditions, while job gains were limited to the health care, construction, and social assistance sectors2.

At the same time, inflation moderated sufficiently to allow the Federal Reserve to continue its gradual path of rate cuts. While inflationary pressures remain a concern, the data to date suggest tariffs have had a minimal impact on overall U.S. price levels3.

Lower interest rates helped support both consumer and corporate balance sheets, boosting spending and investment. Despite persistently weak consumer sentiment surveys, retail spending remained resilient, driven largely by higher-income consumers who benefited from rising home equity and stock market wealth. While spending pressures among lower-income households affected certain sectors, such as fast-food restaurants, stronger demand from more affluent consumers more than offset these effects at the broader economic level.

Supported by solid consumer spending and increased capital expenditures, particularly in AI, real GDP growth accelerated to 4.3% in Q3 2025, up from 3.8% in Q2, and likely remained strong in Q44.

Looking Ahead

As we move into 2026, the tension between a cooling labor market and lingering inflation pressures persists. Nevertheless, both companies and investors have reasons for cautious optimism. Tariffs have not meaningfully impacted economy-wide inflation, in part due to revised and renegotiated headline rates. In addition, the tax legislation passed in 2025 is expected to increase discretionary income for households and corporations, providing further support for economic growth.

As always, markets must navigate numerous uncertainties, including the risk of renewed inflation, a sharper labor market slowdown, potential reassessment of AI-related investments, and ongoing geopolitical tensions. Still, 2025 demonstrated the resilience of companies amid rapid change. While short-term volatility is an inevitable aspect of investing, we believe a diversified global approach remains well-positioned for the long term, and that investors continue to benefit from maintaining disciplined portfolios aligned with their objectives.

Q4 Post-Mortem From an Investment Adviser: Year of Resilience | Kiplinger

https://www.bloomberg.com/news/newsletters/2026-01-13/tariff-pass-through-limited-so-far-us-data-show-evening-briefing-americas

Gross Domestic Product, 3rd Quarter 2025 (Initial Estimate) and Corporate Profits (Preliminary) | U.S. Bureau of Economic Analysis (BEA)

Index Disclosure and Definitions

Investors cannot invest directly in an index. Indexes have no fees. Historical performance results for investment indexes do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment management fee, the occurrence of which would have the effect of decreasing historical performance results. Actual performance for client accounts will differ from index performance.

S&P 500 Index represents the 500 leading U.S. companies, approximately 80% of the total U.S. market capitalization.

Dow Jones Industrial Average (DJIA) Is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange (NYSE) and the NASDAQ.

The Nasdaq Composite Index (NASDAQ) measures all Nasdaq domestic and international based common type stocks listed on The Nasdaq Stock Market and includes over 2,500 companies.

MSCI World Ex USA GR USD Index captures large and mid-cap representation across 22 of 23 developed markets countries, excluding the US. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets (as defined by MSCI). The index consists of the 25 emerging market country indexes. Bloomberg Barclays US Aggregate Bond Index measures the performance of the U.S. investment grade bond market. The index invests in a wide spectrum of public, investment-grade, taxable, fixed income securities in the United States – including government, corporate, and international dollar-denominated bonds, as well as mortgage-backed and asset-backed securities, all with maturities of more than 1 year.

Bloomberg Barclays Global Aggregate (USD Hedged) Index is a flagship measure of global investment grade debt from twenty-four local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging market issuers. Index is USD hedged.

© Morningstar 2021. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied, adapted or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information, except where such damages or losses cannot be limited or excluded by law in your jurisdiction. Past financial performance is no guarantee of future results.

The Kaminsky-Silverman Group utilizes Symmetry Partners, LLC (SP), which is a third-party service provider that supplies market data and assists in creation and monitoring of factor-based investment models. SP is also an investment advisory firm registered with the Securities and Exchange Commission. All data is from sources believed to be reliable but cannot be guaranteed or warranted. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, product or any non-investment related content made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may not be reflective of current opinions or positions. Please note the material is provided for educational and background use only. Moreover, you should not assume that any discussion or information contained in this material serves as the receipt of, or as a substitute for, personalized investment advice.

Diversification seeks to improve performance by spreading your investment dollars into various asset classes to add balance to your portfolio. Using this methodology, however, does not guarantee a profit or protection from loss in a declining market. Past performance does not guarantee future results.

This material is confidential and is provided for informational purposes only and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Investment return and principal value of an investment will fluctuate; therefore, you may have a gain or loss when you sell your investment. Any opinions, expectations and projections within this document are solely those of the Portfolio Manager(s) and/or Financial Advisor(s) identified, and do not necessarily represent the viewpoint of Shufro, Rose & Co., LLC or other Portfolio Managers at the firm. This report was prepared by Shufro, Rose & Co., LLC and is presumed to be correct. Shufro, Rose & Co., LLC is an investment adviser registered with the Securities and Exchange Commission. ADV Part 2A is available upon request or at https://adviserinfo.sec.gov/. Please contact Shufro, Rose & Co., LLC at (212) 754-5100 with any questions.